Kenyans pay nearly double amount for phones in lipa polepole plans; Is it economic?

An illustration photo of a mobile phone user. | FILE/REUTERS

Audio By Vocalize

The Kenya Housing Survey 2023/24 found that a number of Kenyans use mobile phones that they do not own.

While 11.3% of Kenyans use mobile phones that they do not own, the highest reliance on shared or borrowed phones is in urban areas (11.8%) compared to 11.0% in rural areas.

Phone ownership not only enables communication and internet access, but also financial transactions and access to mobile money services.

In its 2024 FinAccess Household Survey, KNBS found that 9.9% of Kenyan adults remain financially excluded due to lack of mobile phones, lack of identity card or poverty. Youth from rural areas account for 45.5% of this financially excluded population.

The survey equally found an increased uptake in Hire purchase plans popularly known as ‘Lipa mdogo mdogo’ or ‘Lipa polepole’.

While 579,242 people had used Lipa polepole services in 2021, the uptake had increased to 1,751,994 in 2024.

The respondents in the survey cite unethical practices as the leading challenge in using Lipa polepole financial services.

The lipa polepole option

Today, if you take a walk through the Nairobi Central Business District (CBD) you are likely to find stalls selling phones. These stalls offer a hire purchase plan for phone buyers who are unable to settle the costs in a one-of payment.

The shops offering these services are also available online and various residencies in Nairobi and other rural towns in Kenya.

This hire purchase plan has been the go-to financial option for a number of Kenyans in informal settlements and rural areas, who lack funds to buy smart phones instantly.

Under this plan, a phone buyer pays an initial instalment for a phone of their choice. They are then given the phone on condition that they will pay between Ksh.50 – Ksh.100 a day for a given period of time. A phone buyer is given a special account number which they use to pay the daily installments through digital wallets like Mpesa.

The traders install mobile applications on the phone to track it and disable its operations whenever a buyer fails to honour the daily remittance agreement. If an instalment is not paid, the phone is automatically locked hence cannot be used by its owner.

David Ochieng, an office messenger in Nairobi has bought two phones through the Lipa polepole scheme.

His first phone was a Samsung Galaxy A12 that he bought at a shop in Nairobi’s GPO area in 2023. Ochieng paid a Ksh.5,000 initial instalment for the phone. He was then required to pay at least Ksh.99 daily until he reaches the Ksh.36,649 mark to own the phone completely.

“The initial payment is not included in the total amount. It is just like giving your money away,” he shares.

Ochieng made daily installments for 3 months, where he paid between Ksh.99 – Ksh.200 to the account depending on the day’s earnings.

When he reached the Ksh.36,649 mark, he was given the green light to own the phone. At the time, the phone costed between Ksh.18,000 – Ksh.20,000 for a one-time purchase. In the hire purchase plan, he paid approximately Ksh.16,649 more.

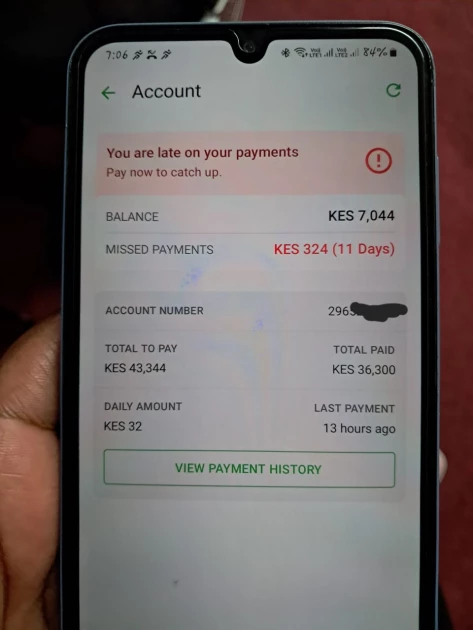

After settling the payment, Ochieng went back to the store in October 2023 to get a Samsung Galaxy A15 for a relative. Under this plan, he made a Ksh.6,500 initial payment and was required to pay a minimum of Ksh.32 daily.

The targeted cost of this phone would be Ksh.43,344, against the market price of Ksh.18,000 – Ksh.22,000. As of mid-January 2025, the phone owner owed the retailer Ksh.7,044 and had defaulted payment for 11 days, hence his phone was disabled.

“When you make your payments in time, you might be given an offer to get another phone even before completing your existing payments,” he explains.

In Eldoret town, Jane Chebet bought a Nokia C32 phone under the Lipa polepole plan in 2024. She paid an initial amount of Ksh.4,500 and is expected to pay Ksh. 90 daily until she reaches the Ksh.36,000 required for her to own the phone.

“In my plan, I was expected to settle the full amount within a year. But I am yet to finish the payment as there are days I would not meet the target,” says Chebet.

The Nokia C32 phone retails for between Ksh.16,000 – Ksh.18,000 in Kenyan shops. This means that under the lipa polepole plan, Chebet will have paid nearly double the retail cost of the phone.

The businesswoman says one of her friends also bought a phone in a lipa polepole plan and has been making payments to the account.

Economics of Lipa polepole

Are these existing hire purchase plans ethical? Are they economical? And what risks do they pose to retailers, who are in the risk of making losses when customers fail to pay for the phones?

Churchill Ogutu, an economist working under IC group says the hire purchase plan offer suitable options for low-income earners who are unable to meet the costs of phones. This is highly dependent on the agreed interest between a retailer and buyer.

“It all depends on affordability. As at the end of the day they pay more than they could have paid in a one-off purchase. But they can not afford the one-off payment. It is a tight balance that they find themselves in,” says Ogutu.

While owning a mobile phone is seen as one of the ways to enhance financial access among low income earners, what stake do the lipa polpole plans have for the financial status of low income earners.

According to Ogutu, such plans might not ultimately improve the financial status of low income earners. He notes that such consumption trends might be detrimental to the financial stability of low income earners.

“The risk is that it does not help you map out your average consumption and expenditure. It tends to distort you because you consume today and pay more for a longer time. That is not the best financial habits to adopt,” the economist adds.

He acknowledges financial risks posed to the retailers. To avoid these, retailers might cushion themselves under the high interest rates. “This is dependent on the stage that buyers default payment. They need to find a win-win mechanism.”

Bridging the digital divide

Majority of people living in rural areas still lack access to internet connectivity and digital devices, hence a broad digital divide among communities.

The divide is mainly due to affordability and access to devices, availability of infrastructure, digital literacy levels and norms that may inhibit some people from adopting digital solutions.

In Kenya today, smart phone users enjoy access to the internet, where they get essential services, digital financial services among other essential services.

While the lipa polepole plans offer an opportunity for access to digital devices, the costs that come with it is also one to look into.

“Yes, it leads to more people having phones, accessing digital products and financial services… but at what cost?” Ogutu poses.

“The best way would be to address the affordability issue as a path towards inclusivity. At the moment, it is still costly,” he opines.

Leave a Comment